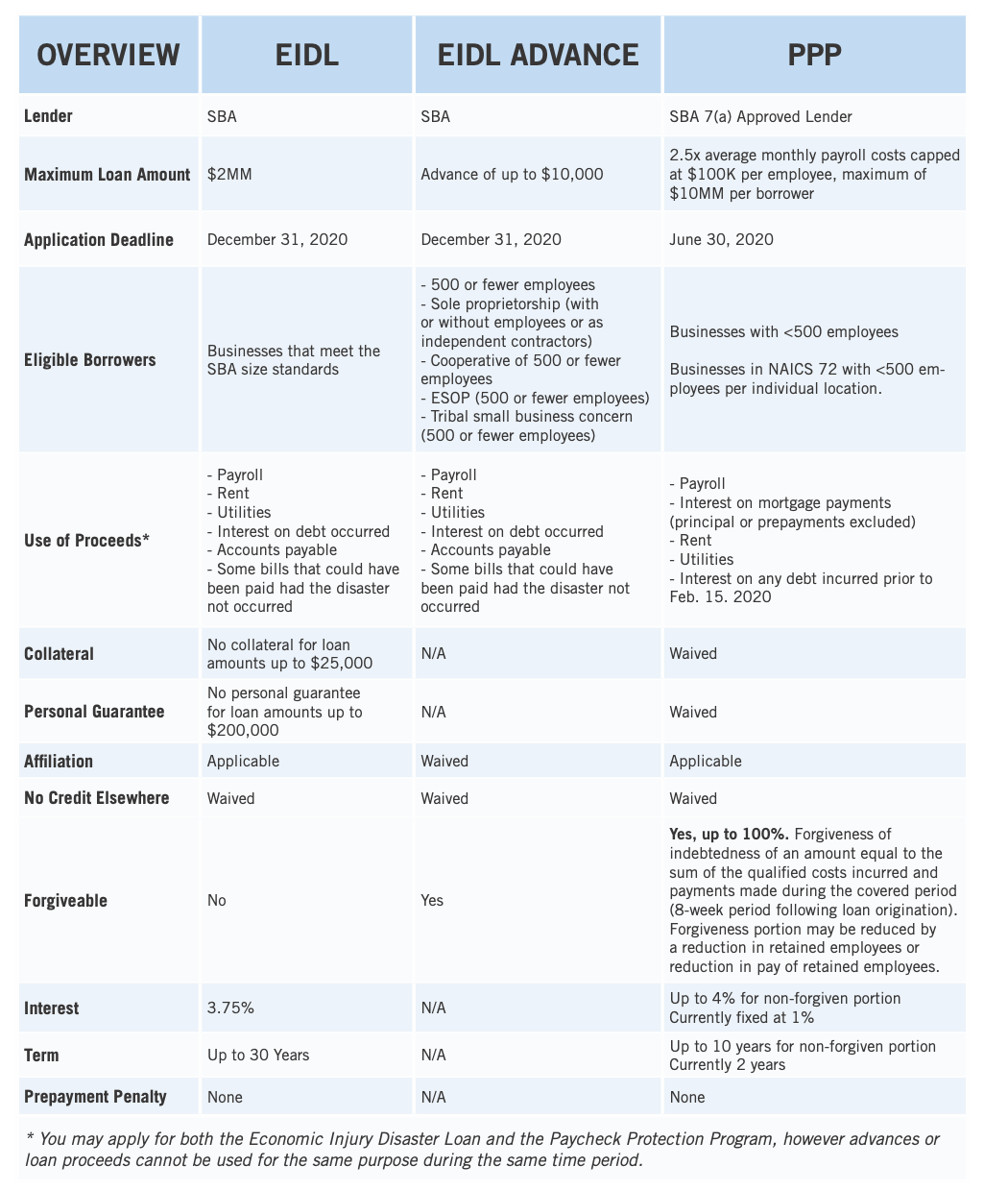

If you are the owner of an S Corporation, how do you calculate what to pay yourself and other shareholders? The Watson CPA Group put together an article on this topic with wonderful illustrations to help you calculate shareholder salaries. Keep reading for an excerpt, or click here for the full article.

If you are the owner of an S Corporation, how do you calculate what to pay yourself and other shareholders? The Watson CPA Group put together an article on this topic with wonderful illustrations to help you calculate shareholder salaries. Keep reading for an excerpt, or click here for the full article.

“Determining a reasonable shareholder salary is the hardest part of running an S corporation. What the heck do I pay myself? Before we get into that, let’s discuss why a reasonable S Corp wage needs to be just above bar napkin quality and just below NASA precision. The Watson CPA Group has been computing officer compensation since 2007, and we believe we have it dialed in as well as anyone can.

Scattered throughout our website and book we’ve stressed that the only tax savings an S Corp provides is the reduction of self-employment taxes, and in the case of S corporation compensation we are talking about Social Security and Medicare taxes (payroll taxes). When your company, or any company, pays you $10,000 in shareholder wages, 7.65% is withheld from your pay check for the employee’s portion of payroll taxes. This is broken down into 6.2% Social Security and 1.45% Medicare. Your company must also pay 7.65% for a combined percentage of 15.3%. Adding on 25% in income taxes equates to a 40% tax rate… yuck!

Therefore, a $10,000 shareholder salary costs you $1,530 in additional taxes beyond income taxes. Said in a different way, if you pay yourself $50,000 when $40,000 could have been a reasonable shareholder salary, you just wasted $1,530. Even a $5,000 delta equates to $765. As such, your S Corp officer compensation needs to be reasonable, sure, but it also needs to be as low as reasonableness and not-so-common sense will allow.

IRS S Corp Stats

Let’s jump right into some numbers first before going through reasonable S Corp salary theory developed from IRS revenue rules and tax court cases. The following table is a summary generated from IRS statistics on S corporation tax returns for the 2013 tax year. Yes, this is the most current. No, we do not know why a room full of servers can’t crunch this in real-time. So here we are-

|

Gross Receipts |

Net Income |

Officer Comp |

Officer Comp % |

| Annual Receipts |

Per Return |

Per Return |

Per Return |

of Net Income |

| $25,000 to $99,999 |

62,552 |

6,672 |

8,871 |

57% |

| $100,000 to $249,999 |

168,051 |

22,194 |

22,786 |

51% |

| $250,000 to $499,999 |

365,476 |

37,732 |

43,158 |

53% |

| $500,000 to $999,999 |

720,013 |

58,351 |

67,474 |

54% |

| $1M to $2.5M |

1,572,621 |

119,808 |

110,911 |

48% |

First some quick observations. Officer compensation is added back to net income to determine officer comp as a percentage of net income. Next, this is all industries from capital intensive manufacturing to personal services business such as attorneys, doctors, consultants, engineers and accountants. Also, this includes S Corps who lost money, and whether they lost money and continued to pay a reasonable shareholder salary (officer compensation) is unclear. In other words, if losses were teased out would officer compensation be reduced as a percentage of net income? We cannot quickly determine.

Here is the same data grouped by gross receipts but detailed by selected industries. First one is $100,000 to $249,999 in gross receipts-

|

Gross Receipts |

Net Income |

Officer Comp |

Officer Comp % |

| $100,000 to $249,999 |

Per Return |

Per Return |

Per Return |

of Net Income |

| Finance and Insurance |

160,359 |

34,408 |

23,213 |

40% |

| Real Estate |

165,375 |

38,231 |

28,193 |

42% |

| Professional, Scientific |

163,151 |

32,910 |

35,404 |

52% |

| Health Care |

174,383 |

24,622 |

36,026 |

59% |

And now for $250,000 to $499,999 in gross receipts-

|

Gross Receipts |

Net Income |

Officer Comp |

Officer Comp % |

| $250,000 to $499,999 |

Per Return |

Per Return |

Per Return |

of Net Income |

| Finance and Insurance |

366,533 |

77,518 |

62,329 |

45% |

| Real Estate |

359,163 |

65,419 |

51,151 |

44% |

| Professional, Scientific |

355,693 |

71,136 |

74,493 |

51% |

| Health Care |

378,147 |

51,553 |

75,382 |

59% |

There you go. Remember that officer compensation includes all fringe benefits such as self-employed health insurance and HSA contributions, and it might be influenced (increased) by those who want to maximize 401k deferrals and / or defined benefits pensions.”